Economic Cycle

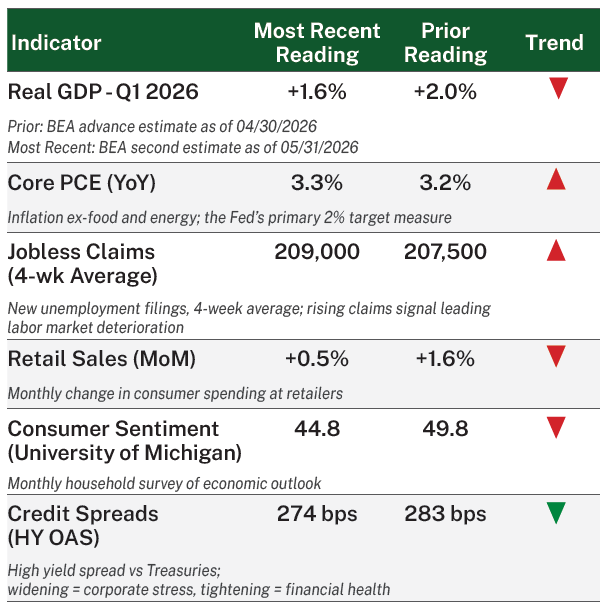

May saw a continued divergence between the economy and markets, as growth showed signs of moderation while markets pushed ever higher. Economic data released during the month suggested the economy entered the second quarter with less momentum than previously believed, as first quarter GDP growth was revised lower and consumer spending growth slowed from earlier estimates.

Despite softer data, labor market conditions remained resilient, providing likely support for consumer spending from here, while easing energy prices as a result of easing geopolitical tensions helped alleviate some of the inflation concerns that emerged earlier in the spring. As a result, markets continued to process the mixed signals of an economy exhibiting slower but resilient growth.

Equity Markets

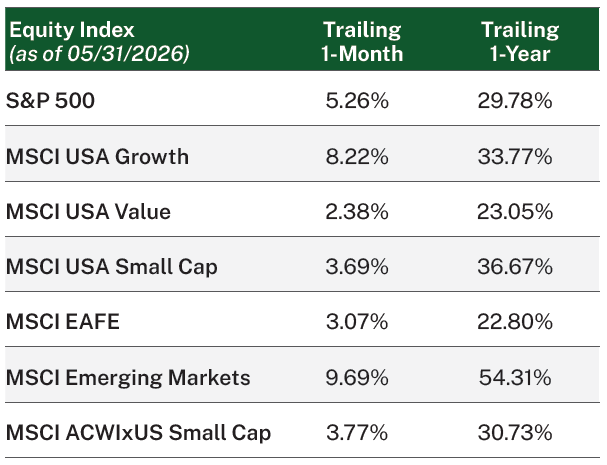

Equity markets extended their advance in May, with the S&P 500 recording a series of new all-time highs throughout the month. In many respects, market leadership and return concentration looked remarkably similar to April, with growth-oriented sectors and large-cap technology companies continuing to drive the majority of gains. Information Technology significantly outperformed every other sector, supported by strong earnings results and continued enthusiasm surrounding artificial intelligence.

Emerging markets also benefited from their exposure to technology and semiconductor supply chains, while mid-cap and small-cap stocks lagged the broader market. Easing geopolitical tensions, meanwhile, had the two-fold effect of Energy sector weakness (on account of falling oil prices) but improved investor optimism helping to support risk appetite more broadly.

Fixed Income Markets

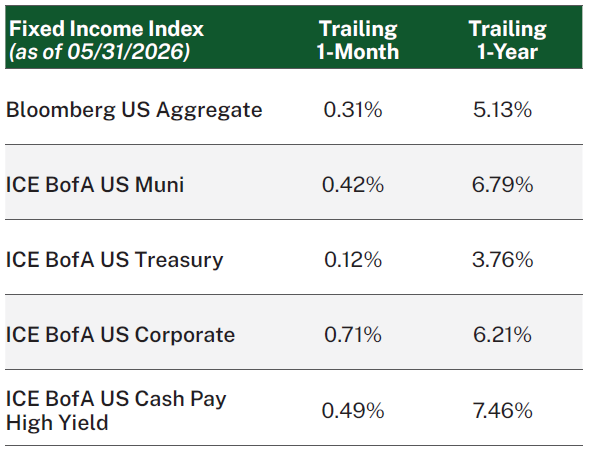

Fixed income markets generated positive returns in May as Treasury yields ended the month only slightly higher across much of the curve. Markets continue to expect the Federal Reserve may need to keep policy tighter for longer on account of inflation concerns, but the move higher in rates was limited as oil prices retreated from earlier highs and inflation concerns surrounding the conflict with Iran began to fade.

Credit markets remained resilient, with tight spreads reflecting healthy corporate fundamentals and continued demand for income-producing assets. Investment-grade corporates modestly outperformed high yield bonds as investors showed a preference for higher-quality issuers amid elevated uncertainty, while municipal bonds also delivered positive returns, supported by attractive tax-exempt yields and continued demand.

Our Perspective

May largely reinforced the market trends that have defined much of 2026. Investors continued to reward companies and industries most closely tied to artificial intelligence and technology spending, while areas of the market more sensitive to the broader economy delivered comparatively muted returns. Strong earnings growth, particularly among large technology companies, has provided support for equities’ continued march upwards despite lingering concerns surrounding inflation, interest rates, and the pace of economic activity.

While the concentrated market leadership driving stock returns bears watching, we continue to maintain a generally constructive outlook on equities. Corporate fundamentals remain strong, though increasingly divergent performance across sectors and market capitalizations reinforces the importance of diversification and valuation discipline.

Within fixed income, elevated yields continue to provide attractive income opportunities across many higher-quality segments of the market. While tight credit spreads warrant selectivity, we believe bonds remain positioned to play an important role in portfolio construction as growth gradually moderates and policy uncertainty persists.

Monthly Recommendation

Acquired (Podcast) Compared to the 30 to 60 minute episodes that dominate most podcast feeds, one of Acquired’s long-form episodes, which typically run between 3 to 4 hours, is a welcome change of pace. Each episode offers a deep, deep dive into one of the world’s greatest companies or organizations – their origin story, their triumphs, and all the tribulations along the way. For any fan of business, markets, or just good stories, a scroll through the Acquired archives and a few hours spent with an episode that catches your eye is time well spent.

Indicator Sources: Bureau of Economic Analysis (BEA) — Q1 Real GDP estimate & Core PCE (bea.gov / fred.stlouisfed.org) | Department of Labor (DOL) Jobless Claims (fred.stlouisfed.org) | Census Bureau Retail Sales (census.gov) | University of Michigan Surveys of Consumers (sca.isr.umich.edu) | ICE BofA High Yield Option-Adjusted Spread (OAS) (fred.stlouisfed.org)

Index Disclosures: Unless otherwise noted, index returns do not reflect any fees or expenses and are provided by Morningstar, Inc. Index data referenced herein is the property of each index sponsor (S&P Dow Jones Indices LLC, a division of S&P Global Inc. (“S&P”), Bloomberg Finance L.P. (“Bloomberg”), ICE Data Indices, LLC (“ICE Data”), and MSCI), their affiliates (“Index Sponsors”) and/or their third-party suppliers and has been licensed for use by Manning & Napier. The Index Sponsors and their third-party suppliers accept no liability in connection with its use. Data provided is not a representation or warranty, express or implied, as to the ability of any index to accurately represent the asset class or market sector that it purports to represent and none of these parties shall have any liability for any errors, omissions, or interruptions of any index or the data included therein. For additional disclosure information, please see: https://go.manning-napier.com/benchmark-provisions. See next page for index definitions.

All investments contain risk and may lose value. This material contains the opinions of Manning & Napier, which are subject to change based on evolving market and economic conditions. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable but not guaranteed.

The S&P 500 Total Return Index is an unmanaged, capitalization-weighted measure comprised of 500 leading U.S. companies to gauge U.S. large cap equities. The index accounts for the reinvestment of regular cash dividends, but not for the withholding of taxes. The MSCI USA Value Index is designed to measure large and mid-cap US securities exhibiting overall value style characteristics. The MSCI USA Growth Index is designed to measure large and mid-cap US securities exhibiting overall growth style characteristics. The MSCI USA Small Cap Index is designed to measure the performance of the small cap segment of the US equity market. The index represents approximately 14% of the free float-adjusted market capitalization in the US. The MSCI EAFE Index is a free float-adjusted market capitalization index designed to measure large and mid-cap representation across 21 Developed Markets countries (excluding the U.S. and Canada). The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets and consists of 24 emerging market country indices outside the U.S. The MSCI ACWI ex USA Small Cap Index is designed to measure a small cap representation across 22 of 23 Developed Markets countries (excluding the U.S.) and 24 Emerging Markets countries. MSCI indices are denominated in U.S. dollars, returns are net of withholding taxes, and they assume daily reinvestment of net dividends thus accounting for any applicable dividend taxation. The Bloomberg U.S. Aggregate Bond Index is an unmanaged, market-value weighted index of U.S. domestic investment- grade debt issues, including government, corporate, asset-backed, and mortgage-backed securities, with maturities of one year or more. Index returns provided by Intercontinental Exchange (ICE). The ICE Bank of America (BofA) U.S. Municipal Securities Index tracks the performance of U.S. dollar denominated investment grade tax-exempt debt publicly issued by U.S. states, territories, and their political subdivisions. Qualifying securities must have at least one year remaining term to final maturity, at least 18 months to final maturity at the time of issuance, a fixed coupon schedule and an investment grade rating. The ICE BofA U.S. Treasury Total Return Index is an unmanaged index that measures the performance of U.S. dollar-denominated, fixed-rate securities issued by the U.S. Treasury across all maturities. The ICE BofA U.S. Corporate Total Return Index is an unmanaged index that measures the performance of U.S. dollar-denominated, investment-grade, fixed-rate corporate debt publicly issued in the U.S. domestic market. The ICE BofA U.S. Cash Pay High Yield Index tracks the performance of U.S. dollar denominated below investment grade corporate debt, currently in a coupon paying period, issued in the U.S. domestic market. Qualifying securities must have at least one year remaining term to final maturity as of the rebalancing date, at least 18 months to final maturity at the time of issuance, a fixed coupon schedule, and a minimum amount outstanding of $250 million.

Morningstar, Inc. is a global investment research firm providing data, information, and analysis of stocks and mutual funds. © Morningstar, Inc. 2026. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied, adapted or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information, except where such damages or losses cannot be limited or excluded by law in your jurisdiction. Past financial performance is no guarantee of future results.